Profit Maximizer

Seasonal Supply Lows Are Here

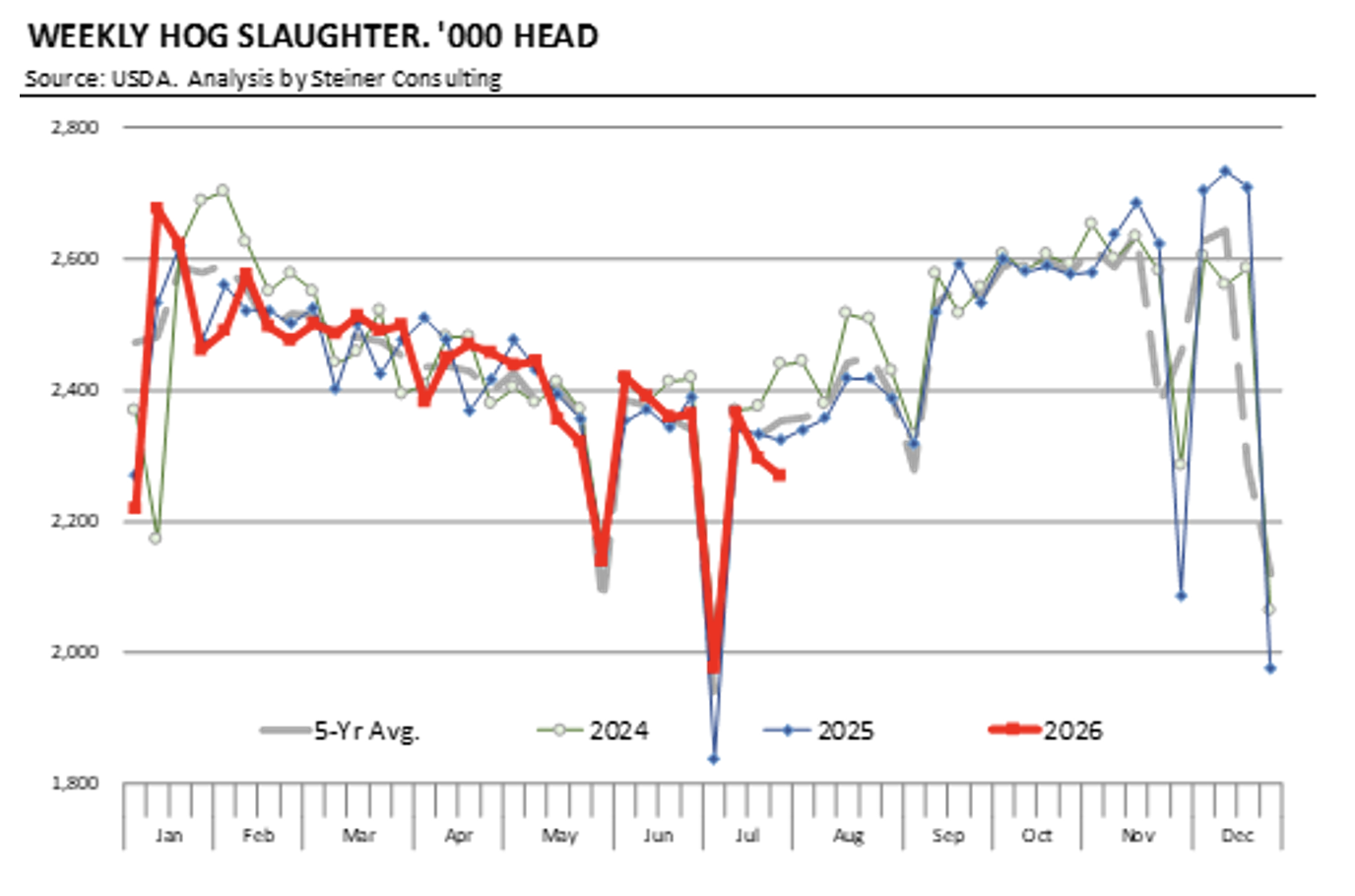

For the second consecutive week, hog slaughter was well below year ago levels. Packers have had disruptions in slaughter both due to maintenance and operational reasons.

The Profit Maximizer is a biweekly report that provides insights and analysis on current pork markets.

Steiner and Company produces the National Pork Board newsletter based on information we believe is accurate and reliable. However neither NPB nor Steiner and Company warrants or guarantees the accuracy of or accepts any liability for the data, opinions or recommendations expressed.

For the second consecutive week, hog slaughter was well below year ago levels. Packers have had disruptions in slaughter both due to maintenance and operational reasons.

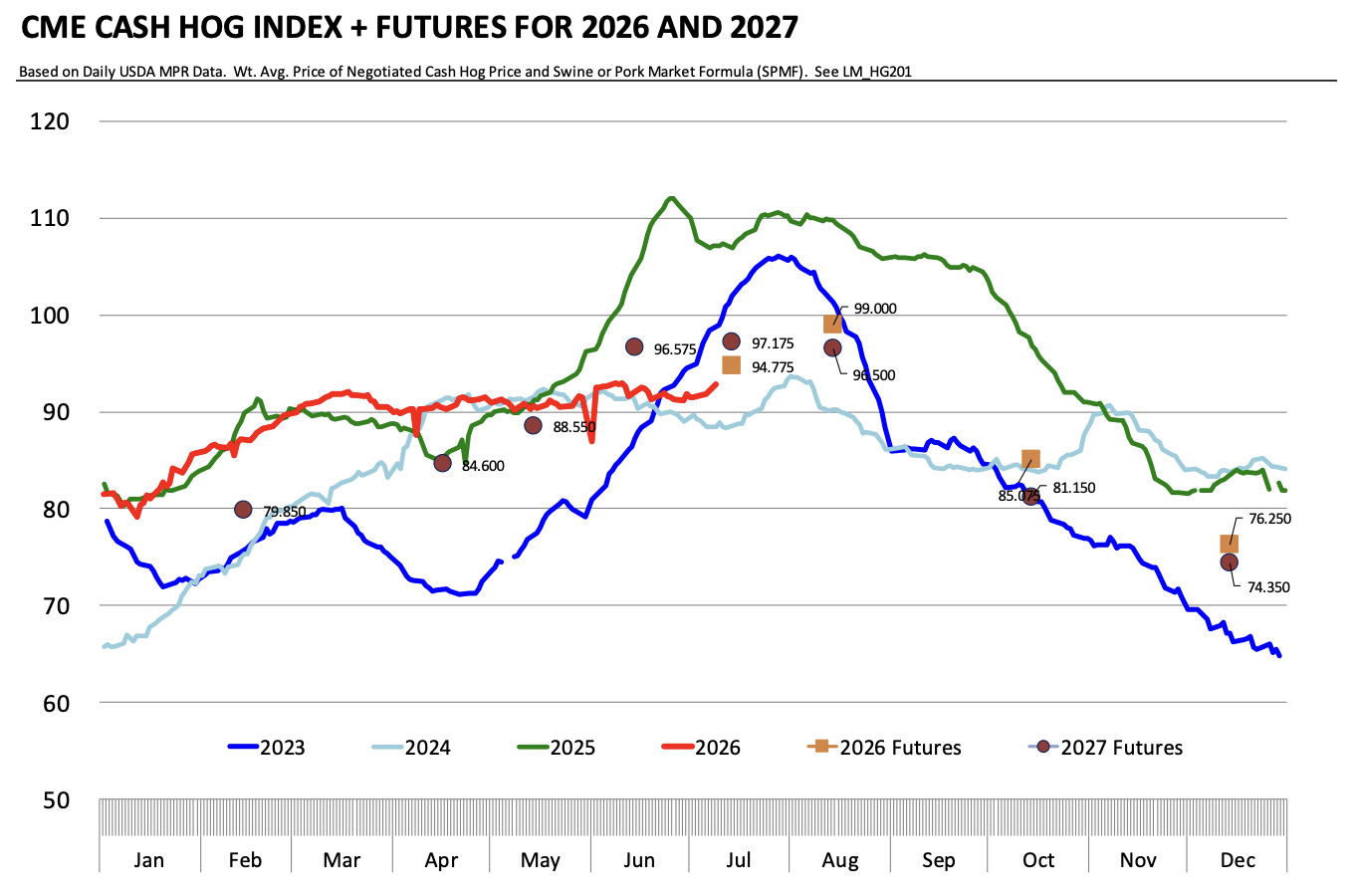

It is not unusual for processing pork prices to rebound after the holidays as plants return to full production schedules. That combined with two short production weeks has resulted in tighter spot availability and higher prices, especially hams.

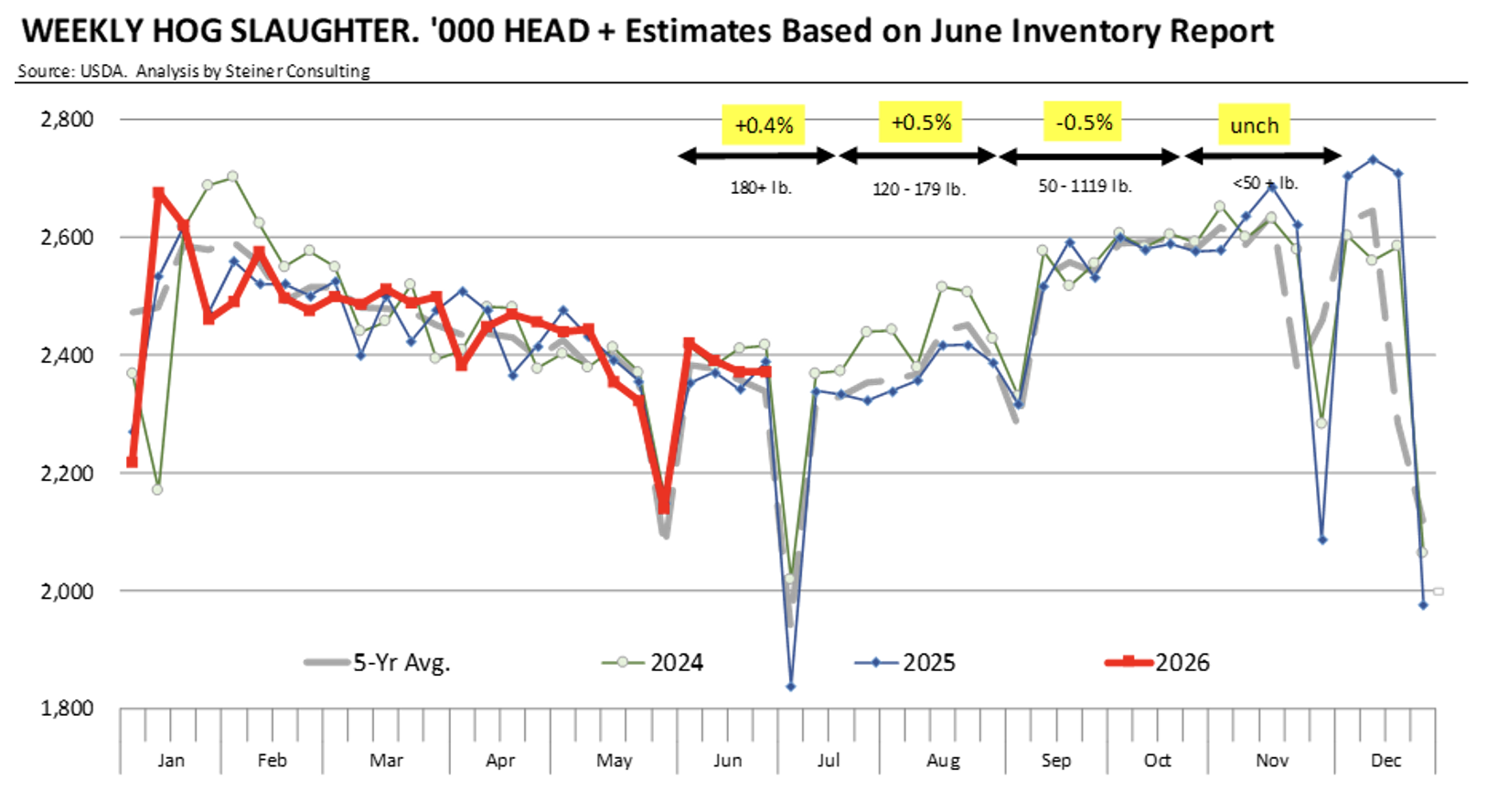

The decline in hog breeding herd will continue to impact growth potential and heighten disease and feed cost risks for 2027.

You’re viewing the website for Pork Checkoff and The National Pork Board.

Find information about sustainability and pork industry ethical principles at porkcares.org.

Find pork cooking inspiration at pork.org.